{kind=link}

Getting a check that you want to pass along to another person can feel confusing the first time you try it. Maybe your landlord accidentally made the rent refund out to you instead of your roommate, or a relative wants you to hand a birthday check straight to your child. Whatever the reason, learning how to endorse a check to someone else is a simple skill once you know the correct wording and where to sign.

This guide walks through every part of the process in plain language, from the exact phrase to write on the back of the check to what happens once the check reaches the new recipient’s bank. You’ll also find bank-specific notes, common mistakes, and answers to the questions people search for most.

What It Means to Sign a Check Over to Somebody Else

When a check is written out to you, you are the only person who can normally cash or deposit it. Signing it over to someone else, sometimes called a third-party endorsement, allows another individual to receive the funds instead of you.

This is different from a regular deposit. A regular deposit only needs your own signature. A third-party endorsement needs your signature plus a short instruction naming the new recipient, which legally transfers your right to collect the money.

The rules for this come from the Uniform Commercial Code section on special indorsement, which most states follow. Under this rule, once you write a person’s name into the endorsement, the check can only be negotiated further by that named person.

When People Sign Checks Over to Family and Friends

There are a handful of everyday situations where signing over a check makes sense:

- Paying back a family member using a check you received

- Passing a rebate, refund, or reimbursement check to a roommate or spouse

- Helping a relative who does not have a bank account nearby

- Correcting a check that was made out to the wrong household member

If you’re learning how to endorse a check to a family member, the process is exactly the same as endorsing it to a stranger or a business. The only difference is that you likely trust the person receiving it, which lowers your fraud risk somewhat, but it does not change the paperwork.

Keep in mind that not every bank accepts these checks anymore. Some institutions have tightened their policies in recent years because signed-over checks are harder to verify than a direct deposit, so it’s worth a quick call to the recipient’s bank before you hand the check over.

The Step-by-Step Process for Signing a Check to Someone Else

Here is the full process broken into manageable steps.

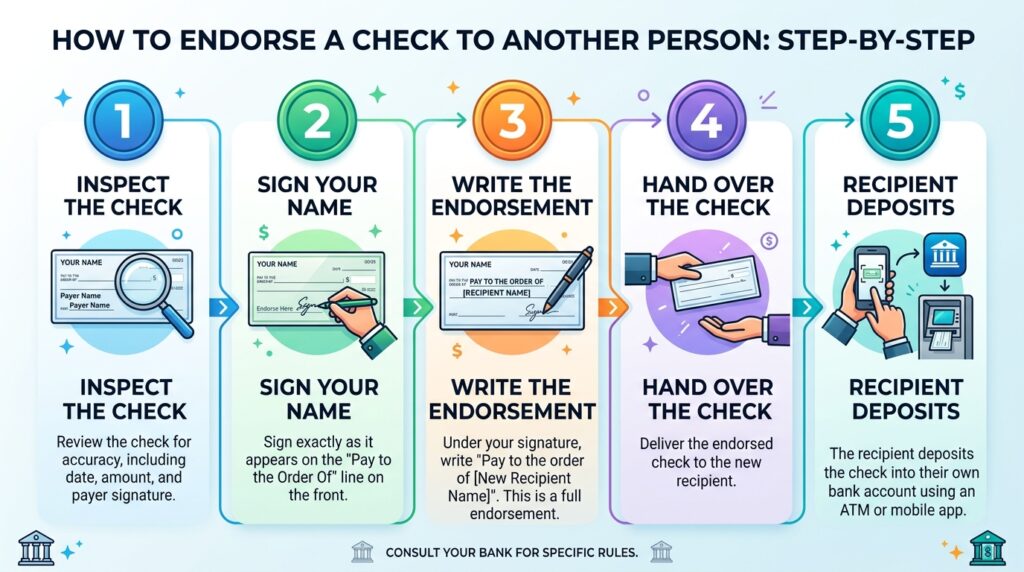

Step 1: Confirm the Check Details First

Before you sign anything, check the date, the dollar amount, and your name on the front. A check that is stale-dated, unsigned by the person who wrote it, or altered in any way may be rejected regardless of how well you endorse it.

Step 2: Flip the Check and Sign Your Own Name

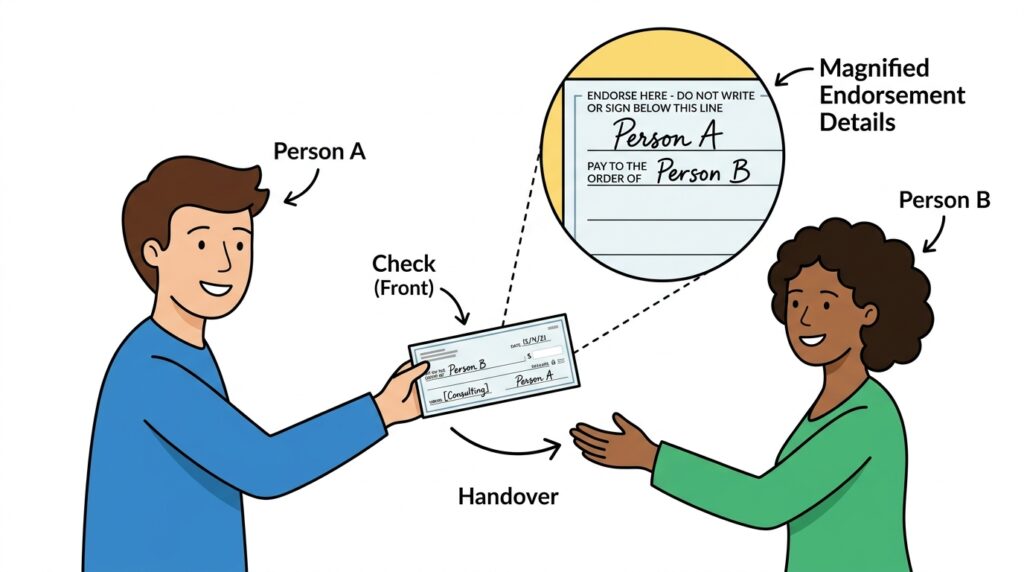

Turn the check over. Near the top of the back, you’ll see a blank line or a shaded box marked for endorsement. Sign your name exactly as it appears in the “Pay to the order of” field on the front. This matters because the signature must match the name in the payee field to confirm you are the intended recipient.

Step 3: Write “Pay to the Order of” Above or Below Your Signature

Directly beneath your signature, write the phrase “Pay to the order of” followed by the full legal name of the person you’re signing the check over to. This is the exact instruction that makes it a valid third-party transfer under the process of taking a physical check written out to you and endorsing another person to cash or deposit it.

Step 4: Hand the Check to the New Recipient

Once both parts are written, the check now legally belongs to the new payee. It’s a good idea to hand it over in person and let the recipient know which bank issued it in case their teller has questions.

Step 5: The Recipient Signs and Deposits It

The recipient then signs their own name underneath yours before depositing or cashing the check. Some banks may also ask the recipient for identification since some banks may require a government issued ID such as a driver’s license or passport when depositing a check on behalf of someone else.

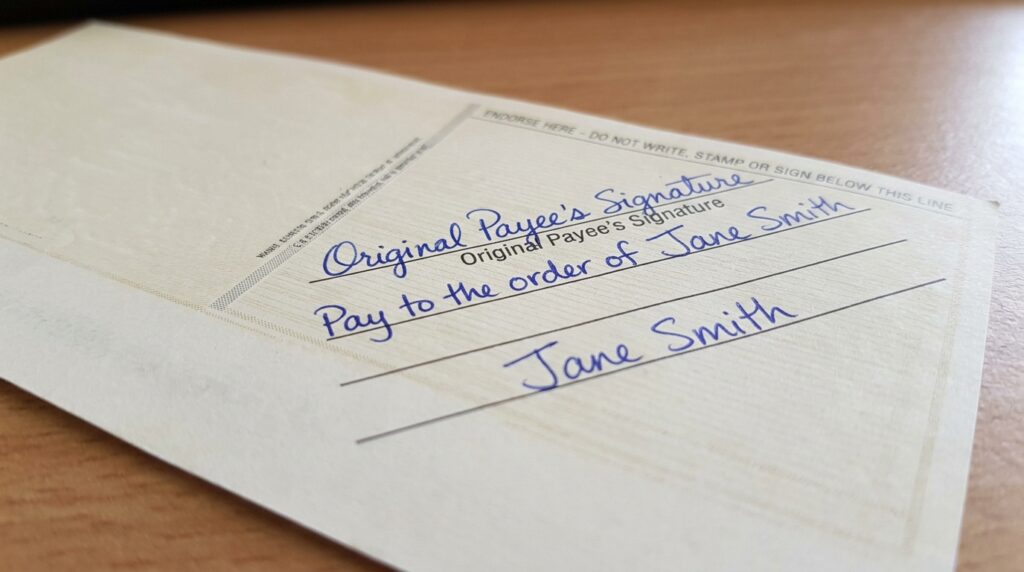

A Real Check Endorsement Example You Can Follow

If you’re searching for a clear check endorsement example, picture the back of the check laid out like this:

| Line | What to Write |

|---|---|

| Top line | Your signature (as the original payee) |

| Second line | “Pay to the order of [Recipient’s Full Name]” |

| Third line (left for recipient) | Recipient’s signature |

This is also a common how to endorse a check to someone else example that banks reference in their own customer guides, including the layout described in writing “Pay to the order of” followed by the new recipient’s name in the endorsement area on the back of the check.

Does the Payee Need to Sign the Back If the Check Isn’t Theirs?

A common question is do I sign the back of a check made out to someone else. The short answer is that only the person named on the front, the original payee, can start the endorsement chain. If a check is made out to your neighbor and you try to sign it yourself without their signature first, most banks will reject it as an improper or forged endorsement.

The Consumer Financial Protection Bureau notes that a check endorsed “for deposit only” by the person it was made out to should prevent anyone else from cashing it, which shows how much weight your endorsement wording actually carries.

Is a Signature Always Required Before Depositing a Check?

Another frequent search is do I have to sign the back of a check to deposit it. In most cases, yes. Some banks now allow “no endorsement required” deposits when the check is going into an account that exactly matches the payee’s name on a bank-branded deposit slip, but this is the exception rather than the rule.

If you skip the signature, expect delays. As one bank explains it, if a check is missing a signature, the bank will generally either refuse to accept it or return it to you.

Handling a Check Written to Two Names

Learning how to endorse a check with two names depends on one small word printed on the front of the check.

- If the check says “John Doe and Jane Doe,” both people must sign the back before it can be deposited or cashed.

- If the check says “John Doe or Jane Doe,” either person can sign alone.

This distinction trips up a lot of people, so it’s worth reading the payee line carefully before assuming only one signature is needed.

The Different Types of Check Endorsements

There are a few standard endorsement styles you’ll come across, and knowing the difference helps you pick the right one.

Blank endorsement: Just your signature, nothing else. It’s the least secure option because anyone who finds the check could cash it.

Restrictive endorsement: Adding “For deposit only” beneath your name. This limits the check so it can only go into a specific account, which is why the restrictive indorsement rule under UCC 3-206 treats words like “for deposit” or “for collection” as a binding instruction on how the check must be handled.

Special (third-party) endorsement: Signing the check over with “Pay to the order of” and a new name, which is the method covered throughout this guide.

Mobile deposit endorsement: Your signature plus a bank-specific phrase, required whenever you’re depositing through an app.

The legal foundation for all of these comes from the definition of an indorsement as a signature, alone or with other words, made on a check for the purpose of negotiating it, restricting its payment, or creating the endorser’s liability on it.

Signing Over a Check at the Big Three National Banks

Bank policies on signed-over checks vary quite a bit, so always confirm with the recipient’s branch before relying on this method.

Third-Party Deposits and How to Endorse a Check to Someone Else Bank of America

If you’re wondering how to endorse a check to someone else Bank of America style, the process follows the standard “Pay to the order of” method described above. Once endorsed correctly, the recipient deposits it the same way as any other check, following the steps in the bank’s own mobile check deposit guide.

Third-Party Deposits and How to Endorse a Check to Someone Else Chase

For how to endorse a check to someone else Chase, the bank’s own instructions confirm that signing over a check means taking a physical check written out to you and endorsing another person to cash or deposit that check, and its official guide on signing over a check walks through the same wording used earlier in this article. Chase also publishes a separate explainer on depositing a check for someone else, which notes that checks marked “for deposit into beneficiary’s account” or “non-negotiable” generally cannot be endorsed to a new person.

Third-Party Deposits and How to Endorse a Check to Someone Else Wells Fargo

For how to endorse a check to someone else Wells Fargo, the bank describes a special or third-party endorsement as a way to sign a payment over to someone else, authorizing that person to deposit or cash the check, and recommends adding “For deposit only” beneath your name for extra security in its check endorsement guide. It’s worth noting that some Wells Fargo branches have grown more cautious about accepting these checks in person, so a quick phone call ahead of time can save a wasted trip.

Mobile Deposit Instructions for a Check Signed Over to You

Once a check has been properly signed over, the new recipient can often deposit it through a banking app rather than visiting a branch, although policies differ by institution.

How to endorse a check to someone else for mobile deposit Chase: After the original payee has signed the check over, the recipient adds their own signature plus the required mobile phrase. Chase’s guidance shows that a mobile check deposit often needs the words “For Mobile Deposit Only” written underneath the signature, though the exact wording can vary by app version.

How to endorse a check to someone else for mobile deposit Bank of America: The recipient signs the back and writes a similar restrictive phrase, since the app typically instructs users to sign the back of the check and include a restrictive endorsement such as “For Mobile Deposit Only to Account at Bank of America”.

Not every bank accepts double-endorsed checks through mobile deposit. Many institutions still require a branch visit for a check that has already changed hands once, largely because a check signed by one person and deposited by another raises fraud concerns since the depositing bank has to guarantee that the earlier endorsement was genuine.

Depositing vs Cashing a Signed-Over Check

There’s a meaningful difference between how to endorse a check to someone else for deposit and how to endorse a check to someone else to cash.

For a deposit, the recipient typically needs an account at the bank the check is being deposited into, and the funds usually take a day or two to become available.

For cashing, the recipient walks into a branch (often the branch the check was drawn from) and receives money immediately, though they may be charged a fee if they don’t have an account there. Some banks refuse to cash third-party checks over the counter at all, since the restrictive endorsement rules discussed earlier were written specifically to limit that kind of transaction.

If speed matters more than convenience, cashing is usually faster. If security matters more, depositing into a verified account is the safer route.

The Legal Rules Behind Every Check Endorsement

Understanding check endorsement rules and regulations helps explain why banks are sometimes strict about accepting signed-over checks.

Under the Uniform Commercial Code’s indorsement rules, an endorsement is legally defined as any signature made for the purpose of transferring, restricting, or accepting liability on a check. Once you write another person’s name into that endorsement, the check becomes payable only to that identified person and can only be negotiated further through their own endorsement.

The Consumer Financial Protection Bureau also offers protection if an endorsement is forged, noting that a consumer is generally not responsible for a fraudulent endorsement as long as they report it within the timeframe set by state law. That said, these federal and state protections work best when the original endorsement was done correctly in the first place, which is exactly why getting the wording right matters so much.

Reasons Banks Reject Third-Party Checks

Even a correctly signed-over check can bounce back at the counter. Common culprits include:

- The recipient’s bank simply does not accept signed-over checks as a matter of policy

- The signature does not match the name printed in the payee field

- The check is more than six months old, since most banks won’t cash or deposit a check that is more than six months old

- The check already carries a restrictive endorsement like “for deposit only,” which under UCC 3-206 legally blocks anyone other than the named bank or account from collecting on it

- Missing identification from the new recipient at an in-person deposit

If a bank refuses the check, the safest fallback is usually to ask the original check writer for a new check made directly out to the intended recipient.

Expert Tips for a Smooth Hand-Off

A few small habits go a long way toward avoiding a rejected check:

- Call the recipient’s bank first to confirm they accept third-party checks at all

- Wait until you’re both ready to complete the transaction before signing anything, since an endorsed check that gets lost is far riskier than an unsigned one

- Use blue or black ink only, and keep your signature within the printed endorsement box

- Bring identification along if the recipient is depositing in person, since some branches ask both parties to appear

- Consider a restrictive endorsement plus the new name together, such as “Pay to the order of [Name], for deposit only,” for extra protection

Weighing the Pros and Cons

| Pros | Cons |

|---|---|

| Avoids the delay of depositing and then transferring money separately | Not all banks accept signed-over checks anymore |

| No fees involved, unlike a wire transfer or money order | Raises fraud risk if the check is lost after endorsement |

| Works well for trusted family situations | Recipient may still need to show ID or visit a branch |

| Legally recognized process under the UCC | Some banks require both parties present in person |

Frequently Asked Questions

Can I endorse a check to someone else without their knowledge?

No. The recipient generally needs to know the check exists and provide their own signature before a bank will accept it. Endorsing on someone’s behalf without permission can be treated as a forged endorsement.

What if the recipient’s bank refuses the signed-over check?

Ask the original issuer to void the check and reissue a new one directly in the recipient’s name. This avoids the third-party endorsement problem entirely and tends to process faster.

Is there a limit on how many times a check can be signed over?

Most banks only accept a single third-party endorsement. A check that has already been signed over once and is being signed over again is far more likely to be rejected.

Do I need to write “for deposit only” when signing a check over?

It’s optional but recommended. Adding that phrase after the new payee’s name limits the check to deposit only, which adds a layer of protection if it’s misplaced before it’s cashed.

Can a business check be signed over to an individual?

Sometimes, but it depends on the bank and whether the business check includes restrictive language. Many business checks are pre-printed with “for deposit only,” which blocks a third-party endorsement entirely.

Final Thoughts

Signing a check over to someone else is a straightforward process once you understand the wording banks expect to see. Sign your name as it appears on the front, write “Pay to the order of” followed by the new recipient’s full name, and let that person add their own signature before depositing or cashing it.

Because policies differ so much between banks, and even between branches of the same bank, the smartest first move is always a quick phone call to confirm the recipient’s bank will accept a signed-over check before you rely on it.

If you found this guide helpful, consider sharing it with anyone who might be handed a check that isn’t quite in their name yet.

This article is for informational purposes only and does not constitute legal, tax, or financial advice. Bank policies change frequently, so always confirm current requirements directly with your financial institution before acting on any information here.