{kind=link}

Leasing a car always sounds simple until your life changes faster than your contract does. A new job, a growing family, a move overseas, or just a budget that no longer fits the monthly payment can leave you stuck wondering how to get out of a car lease early without penalty.

The good news is that you are not actually trapped. Most lease agreements include exit paths, and thousands of drivers in the United States, the United Kingdom, and Canada walk away from leases every year without paying the full early termination fee. This guide breaks the process down in plain, beginner-friendly language so you can pick the option that fits your situation, wherever you live.

Why Car Leases Are So Hard to Exit Early

A lease is not a loan. It is a long-term rental agreement, and the leasing company prices it based on how much the car is expected to depreciate over the full term. When you stop the agreement early, the company loses out on the depreciation income it was counting on, and that is exactly what an early termination fee is meant to cover.

This is why leasing companies rarely let you simply hand back the keys and walk away. They want their projected revenue, one way or another, and the contract you signed gives them the legal right to collect it.

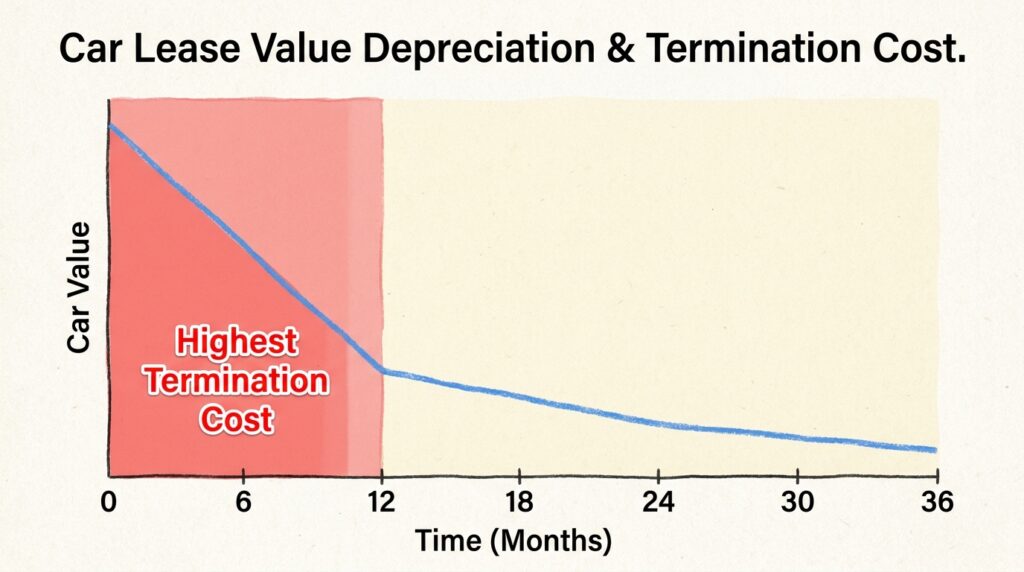

How Depreciation Drives Early Termination Costs

Depreciation is steepest in the first year or two of ownership, which is also when leasing companies are most exposed if you exit early. That is why ending a lease in month six almost always costs more than ending it in month thirty.

If you are weighing whether now is the right time, it helps to know that waiting even a few months can sometimes meaningfully lower your exit cost, simply because less depreciation remains unpaid.

Common Reasons Drivers Want Out of a Lease Early

Understanding why people typically need to exit early can help you figure out which exit strategy fits your own circumstances, since some reasons open doors that others do not.

A job relocation, especially overseas, often qualifies for special handling that a simple change of heart would not. Financial hardship, such as a layoff or unexpected medical expense, tends to make leasing companies more willing to negotiate. A growing family that no longer fits the vehicle, exceeding the agreed mileage allowance, or simply losing interest in the car are also extremely common triggers.

- Job relocation or a new role requiring a company vehicle

- Financial hardship, including job loss or reduced income

- Family changes, such as a new baby or a larger household

- Driving far more miles than the lease allows

- Vehicle no longer suits your lifestyle or needs

Whatever your reason, documenting it clearly before you contact your leasing company can strengthen your position, particularly if you plan to ask for a reduced fee.

Job Relocation and Overseas Moves

Relocating for work, particularly to another country, is one of the strongest cases for a smoother lease exit. Many leasing companies have specific procedures for relocation requests, and in the US, active-duty military relocations carry additional legal protections, which is covered in more detail later in this guide.

If relocation is your reason, gather your offer letter or relocation notice early, since most leasing companies will ask for documentation before approving any special terms.

Financial Hardship and Income Changes

A sudden drop in income changes what you can realistically afford, and leasing companies generally understand this far better than people expect. Many will offer a payment plan, a temporary deferment, or a reduced settlement rather than pushing a struggling customer toward default, simply because collections and repossession cost them money too.

If hardship is your situation, reach out before you miss a payment rather than after, since your negotiating position is almost always stronger when you are proactive.

Your Main Options for Ending a Lease Early

Before diving into country-specific rules, it helps to understand the handful of strategies that work almost everywhere. Each one has different costs, timelines, and levels of effort, so think of this as your menu of choices.

| Option | Typical Cost | Speed | Credit Impact |

|---|---|---|---|

| Lease transfer or swap | Low (transfer fee only) | 2 to 6 weeks | Minimal if done properly |

| Lease buyout and resale | Moderate to high upfront | 1 to 2 weeks | None if paid in full |

| Trade-in for a new lease | Rolled into new payments | Same day | None if approved |

| Direct negotiation | Variable, often reduced | Days to weeks | Minimal |

| Early return or surrender | Highest | Immediate | Can be significant |

Option 1: Transfer or Swap Your Lease

A lease transfer, sometimes called a lease assumption or lease swap, lets another driver take over your remaining payments and the vehicle itself. You step out of the contract, and the new lessee steps in, usually with the leasing company’s approval.

This is widely considered the cheapest way to handle early lease termination because you typically only pay an administrative transfer fee instead of the full penalty. In the United States, marketplaces like Swapalease and LeaseTrader connect people who want out of a lease with people who want a short-term lease, making it easier to find a qualified match.

Keep in mind that not every leasing company allows transfers. Some brands restrict them entirely, while others require the new lessee to pass a credit check before approving the swap.

Option 2: Buy Out the Lease and Sell the Car

Most leases include a buyout clause that lets you purchase the vehicle for a pre-agreed price before the term ends. If the car’s current market value is higher than that buyout price, you can sell it privately or to a dealership and pocket the difference, or at least offset most of your exit costs.

A quick way to check this is to compare your buyout quote against your car’s resale value using a trusted valuation tool before committing. Used car prices fluctuate, so a buyout that made no sense a year ago might be a smart move today.

Option 3: Trade In for a New Lease

If you still want a vehicle but not the one you currently have, many dealerships will roll your remaining lease balance into a new lease. This is sometimes marketed as a lease pull-ahead program, where the dealer forgives a portion of your remaining payments in exchange for starting a fresh contract with them.

This route gets you out of the old commitment quickly, but it usually increases your new monthly payment, so it is worth running the numbers carefully before signing anything.

Option 4: Negotiate Directly With the Leasing Company

It sounds simple, but a direct, honest conversation with your leasing company can sometimes reduce your penalty more than you expect, especially if you can point to financial hardship, job relocation, or a documented life change.

Leasing companies often prefer a negotiated settlement over the cost and hassle of repossession or collections, so there is more flexibility here than most people assume. Always ask for any agreement in writing before you stop making payments.

Option 5: Return the Vehicle (Last Resort)

Simply returning the car and walking away is technically possible, but it is almost always the most expensive route. You may owe the remaining balance, a termination fee, and the gap between the car’s current value and its expected residual value.

This option should generally be considered only when transfers, buyouts, and negotiation are not realistic, since it carries the highest financial and credit risk of all the strategies covered here.

How Leasing Companies Calculate Your Early Termination Fee

Knowing the math behind your termination quote makes it much easier to spot whether a number seems fair or inflated. Most leasing companies follow a similar formula, even though the exact terminology differs by country.

In general, your fee is based on the gap between what you still owe under the contract and what the leasing company can recover by selling or appraising the vehicle today. That gap typically includes three components: your remaining contractual payments, the difference between the car’s current value and its originally projected residual value, and any administrative or disposition fees written into your agreement.

Worked example: Imagine a lease with 18 months of payments remaining at $400 a month, for a total of $7,200. If the leasing company appraises the car at $2,000 less than its expected residual value, and charges a $395 disposition fee, your estimated termination cost would land somewhere in the range of $2,395 to $4,395, depending on how the contract treats the remaining payments versus the depreciation gap.

This is exactly why a written, itemized termination quote matters so much. Without one, it is almost impossible to check whether the number you have been given actually matches your contract’s own formula.

How to Get Out of a Car Lease Early in the USA

In the United States, lease terms are governed in part by the federal Consumer Leasing Act, which requires leasing companies to clearly disclose early termination costs before you ever sign. This means your contract should already spell out exactly what you would owe if you exit early.

Most American drivers who successfully exit a lease early use one of three paths: a lease transfer, a buyout followed by resale, or a negotiated settlement with the leasing company. According to consumer finance guidance, getting out of a car lease early typically involves paying the difference between what you owe and what the leasing company can recover when it resells or appraises the vehicle.

Lease Transfer Marketplaces in the USA

If a transfer fits your situation, online marketplaces have made the process far more accessible than it used to be. Listing your vehicle, sharing payment details, and connecting with interested drivers can usually be done from your phone in under an hour.

Just remember that leasing companies, not the marketplaces themselves, ultimately approve or deny the transfer, so it is worth contacting your lender directly before you commit time and money to a listing.

Military Protections Under the SCRA

Active-duty service members have a unique legal advantage when it comes to ending a lease early. Under the Servicemembers Civil Relief Act, eligible service members can terminate an auto lease without paying the usual early termination charges, provided they meet specific conditions such as being called to active duty for 180 days or more, or receiving a permanent change of station order.

To use this protection, you typically need to send written notice along with a copy of your military orders to the leasing company. You may still owe certain outstanding fees, such as excess mileage or unpaid taxes, but the early termination penalty itself is waived.

Federal Consumer Protections on Lease Disclosures

The Consumer Leasing Act requires lessors to disclose early termination terms clearly before you sign, which means you have the right to know your potential exit costs from day one. If your contract is vague or your leasing company refuses to provide a clear termination quote, that disclosure requirement gives you grounds to push back.

This protection will not waive your fees, but it does mean you are entitled to transparent numbers before deciding which exit strategy makes sense.

How to End a Car Lease Early in the UK

Car leasing in the UK works a little differently, and the terminology can be confusing for beginners. Personal Contract Hire, often just called leasing, is treated separately from Personal Contract Purchase and Hire Purchase finance agreements, and the exit rules differ between them.

For a standard lease, most providers offer a short cooling-off window at the start, followed by a formal early termination process with a fee attached for the rest of the term. For finance agreements like PCP and HP, UK law gives you a stronger built-in right to walk away once you have paid a certain percentage of the total cost.

This distinction trips up a lot of first-time leasers, so before you do anything else, check the heading on your paperwork. If it says Personal Contract Hire or simply Contract Hire, you are dealing with a pure lease and the voluntary termination right described below will not apply. If it says Personal Contract Purchase or Hire Purchase, you likely have stronger legal options for an early, penalty-light exit.

The 14-Day Cooling-Off Period

Most UK lease agreements include a 14-day cooling-off period after signing, during which you can cancel without paying a penalty. If your circumstances change almost immediately after taking out the contract, this is by far the simplest and cheapest exit available.

Once those 14 days pass, ending the agreement typically requires paying a termination charge, often calculated as 50 percent or more of your remaining payments, so timing really does matter here.

Voluntary Termination Rules for Car Finance

If your vehicle is on Personal Contract Purchase or Hire Purchase finance rather than a pure lease, UK consumers have a legal right called voluntary termination. Once you have paid at least 50 percent of the total amount payable, you can cancel the agreement and return the vehicle without owing the remaining balance.

This right comes from the Consumer Credit Act, and finance companies cannot refuse a valid request. It is worth noting that voluntary termination applies to finance agreements rather than standard contract hire leases, so check which type of agreement you actually have before assuming this applies to you.

BVRLA Fair Wear and Tear Standards

Whenever you return a leased vehicle in the UK, whether early or at the natural end of the term, it will be checked against an industry-wide condition standard. The BVRLA Fair Wear and Tear Guide explains what counts as normal deterioration versus chargeable damage, covering everything from tyre wear to interior stains.

Reviewing this guide before your handover date and fixing minor issues yourself is usually far cheaper than letting the leasing company charge you for repairs after collection.

How to Get Out of a Car Lease Early in Canada

Canadian lease agreements share many similarities with their US counterparts, but the exit landscape has its own well-known marketplaces and dealer practices worth understanding before you start the process.

Breaking a lease early in Canada generally comes with a termination fee plus a charge tied to the vehicle’s depreciation, but as with the US and UK, transferring the lease to someone else is usually the most affordable path out.

Provincial rules and individual leasing company policies can also affect your options, so it is worth confirming details with your specific lender. Some manufacturers restrict transfers within the first several months of a new lease, while others place no restrictions on timing at all, which is one more reason to read your contract before assuming a transfer will work the way you expect.

Lease Takeover Marketplaces in Canada

Canada has a long-running, well-established lease takeover industry. Platforms such as Leasebusters have operated since the early 1990s and specialize in matching Canadian drivers who want out of a lease with drivers looking for a shorter-term commitment.

Using a dedicated takeover marketplace can help you avoid the steep termination and deficiency fees that come with simply returning the car, since the new lessee assumes responsibility for the remaining payments instead.

Dealer Buybacks and Positive Equity

Used vehicle values have shifted significantly in recent years, and that has changed the math for many lease holders. Some dealers will now buy out your remaining lease early, sometimes even paying you cash, if your vehicle’s market value comfortably exceeds the payout amount, according to consumer advocates writing on the topic for the Globe and Mail.

It is worth shopping your car around to a few dealers rather than only asking the one you originally leased from, since offers can vary considerably between dealerships.

Why Exiting a Lease Costs More Than Exiting a Loan

It helps to understand why leases are tougher to escape than a typical auto loan, since the comparison explains a lot about the fees you are facing.

With a loan, you already own the car, so paying it off early simply transfers ownership to you free and clear, and many lenders do not even charge a prepayment penalty. With a lease, you never owned the vehicle in the first place. The leasing company is the legal owner, and your monthly payment was essentially rent calculated against a very specific depreciation curve and timeline.

Ending that arrangement early breaks the financial model the leasing company built the entire contract around, which is the core reason early termination fees exist at all. Loans are priced around interest, while leases are priced around depreciation and residual value, and that single difference explains almost every quirk in how exit costs are calculated.

This distinction matters when you are deciding between a buyout and a straight return. Once you buy out the lease, you are effectively converting it into ownership, which is why buyout exits often feel more financially predictable than walking away empty-handed.

Will Ending a Lease Early Hurt Your Credit Score?

This is one of the most common worries people have, and the honest answer is that it depends entirely on how you exit. If you pay off the agreed termination amount in full and the leasing company reports the account as settled, the impact on your credit is usually minimal.

The real credit risk comes from missing payments, defaulting, or having the vehicle repossessed. Those events are reported negatively and can stay on your credit file for years, which is why communicating with your leasing company before you fall behind matters so much.

A properly handled lease transfer is usually the gentlest option for your credit file, since you are formally released from the contract once the new lessee is approved. A negotiated early termination, paid in full, generally shows up as a closed account in good standing rather than a default. Voluntary surrender, missed payments, or repossession are the scenarios most likely to cause lasting damage, sometimes affecting your credit for several years.

If you are unsure how a particular exit option will be reported, it is reasonable to ask your leasing company directly how the account will appear on your credit file once the process is complete, and to get that answer in writing if possible.

Pros and Cons of Each Exit Strategy

Every option discussed in this guide trades cost against convenience in a different way. Use this quick comparison to see which strategy best matches your priorities, whether that is saving money, saving time, or protecting your credit.

There is rarely a single right answer here. A driver facing financial hardship might prioritize speed over cost savings, while someone simply bored with their current car might be willing to wait several weeks for a transfer that saves them thousands. Reviewing the table below alongside your own timeline and budget should make the decision much clearer.

| Strategy | Pros | Cons |

|---|---|---|

| Lease transfer | Lowest cost, minimal credit impact | Takes time to find a buyer; not all leases allow it |

| Lease buyout | You gain an asset to resell | Requires upfront cash or financing |

| Trade-in | Fast, gets you into a new vehicle | Higher new monthly payment |

| Direct negotiation | Can reduce fees significantly | Outcome is not guaranteed |

| Early return | Quickest exit | Most expensive, biggest credit risk |

Expert Tips to Minimize Costs When Exiting a Lease

A few small habits can make a real difference to how much you ultimately pay, no matter which exit route you choose.

- Re-read your lease contract in full before contacting your leasing company, so you already know your rights and rough costs.

- Get a written termination quote rather than relying on a verbal estimate from a call center.

- Check your car’s current resale value before deciding between a buyout and a straight return.

- Keep mileage and vehicle condition in mind well before your planned exit date, since both directly affect your final bill.

- Always confirm any negotiated agreement in writing before you stop making payments.

- Compare quotes from more than one dealer if you are considering a trade-in or dealer buyback, since offers can vary by hundreds or even thousands of dollars.

- Time minor repairs before your inspection rather than after, since fixing small scratches or dents yourself is almost always cheaper than letting the leasing company handle it.

- Ask whether your specific contract allows transfers before paying any listing fees on a marketplace, since not every leasing company permits them.

Acting earlier rather than later almost always works in your favor, since depreciation and accumulated fees only grow the longer you wait. Treat your first phone call to the leasing company as a fact-finding mission rather than a final decision, and you will usually end up with a clearer, cheaper path forward.

Key Lease Terms Worth Knowing

A handful of terms show up again and again in lease contracts and exit conversations. Understanding them before you call your leasing company can save you time and help you ask sharper questions.

- Residual value: The amount the leasing company expects the car to be worth at the end of the term, used to calculate your monthly payments.

- Early termination fee: The penalty charged for ending the lease before the agreed term, usually tied to remaining payments and depreciation.

- Buyout price: The amount required to purchase the vehicle outright before the lease ends, including residual value and remaining obligations.

- Lease assumption or transfer: Another driver formally taking over your remaining payments and the vehicle itself.

- Disposition fee: An administrative charge applied when the vehicle is returned, separate from depreciation-related costs.

- Voluntary termination: A UK legal right allowing certain finance agreements to be ended once 50 percent of the total cost has been paid.

Keeping these definitions handy makes it much easier to read your own contract critically rather than simply accepting whatever number you are first quoted.

Frequently Asked Questions

Is it possible to get out of a car lease without paying any fees at all?

It is uncommon to avoid every fee entirely, but a clean lease transfer often limits your cost to a small administrative charge instead of the full early termination penalty, which is the closest most drivers get to a fee-free exit.

How much does it typically cost to break a car lease early?

Costs vary widely depending on your contract, remaining term, and the car’s depreciation, but early termination fees can range from a few hundred dollars or pounds up to several thousand if you exit very early in the agreement.

Can I just stop making payments and return the car?

You should not do this. Stopping payments without informing your leasing company can trigger repossession, default fees, and serious credit damage, so always communicate first, even if you cannot afford to continue.

Does transferring my lease affect my credit score?

A properly completed lease transfer, where the leasing company formally removes you from the contract, typically has little to no negative effect on your credit, since you are no longer responsible for future payments.

What is the cheapest way to get out of a lease in most cases?

For the majority of drivers across the US, UK, and Canada, a lease transfer or takeover tends to be the most affordable option, since it shifts the remaining payments to a new lessee instead of requiring you to pay a lump-sum penalty.

Final Thoughts

Being stuck in a car lease that no longer fits your life is stressful, but it is rarely a dead end. Whether you are in the United States, the United Kingdom, or Canada, the same general principle applies: transferring the lease is usually your cheapest path out, a buyout makes sense when your car has equity, and direct, early communication with your leasing company almost always beats silence.

It also helps to remember that leasing companies deal with early exits constantly. You are not the first driver to call them with a change in circumstances, and most have established processes for exactly this situation, even if their first quoted number is not their final offer. Asking questions, requesting things in writing, and comparing more than one option before committing puts you in a far stronger position than simply accepting the first figure you are given.

Take a few minutes today to pull out your contract, check your numbers, and decide which option fits your situation best. The sooner you act, the more choices you typically have, and the less the whole process tends to cost. If your circumstances are complicated, such as a pending move, a financial hardship, or a dispute over fees, it is always worth a short conversation with your leasing company or a qualified advisor before signing anything new.

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or credit advice. Lease terms vary by company, contract, and country, so always review your own lease agreement and speak with your leasing company or a qualified advisor before making a decision.